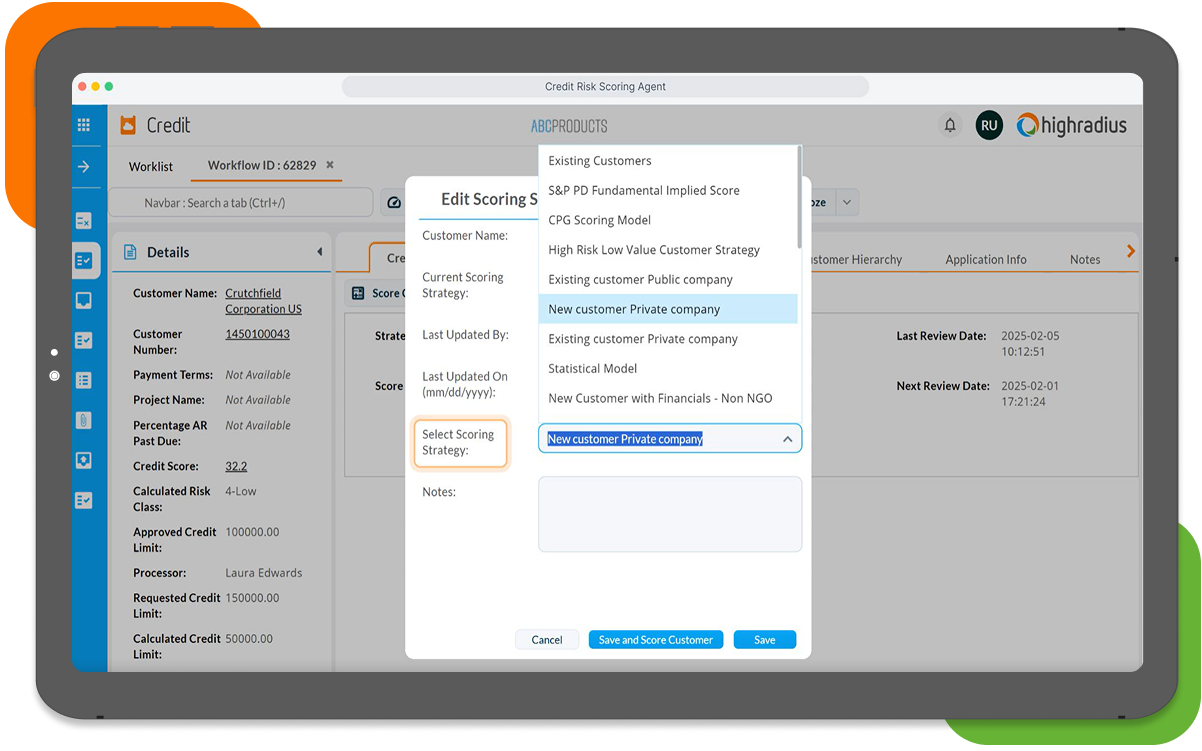

Automated Credit Scoring Software for Smarter Credit Risk Evaluation

80% automated risk evaluations | 50% faster credit limit decisions

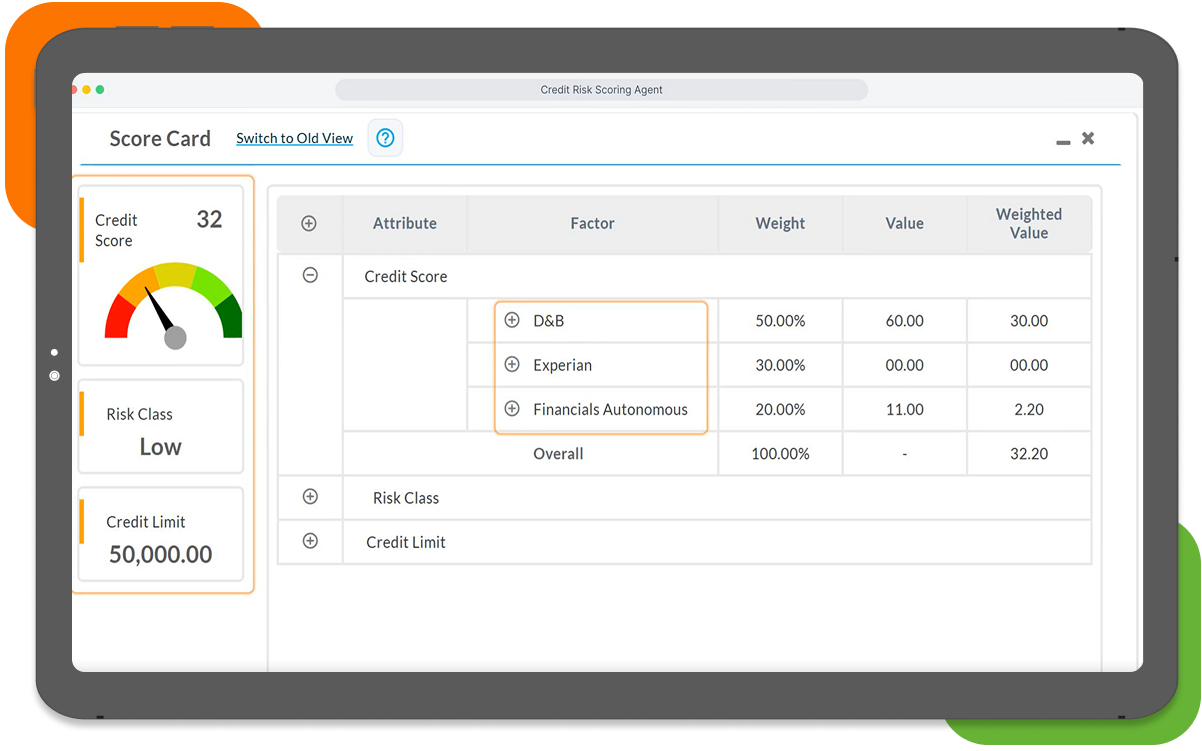

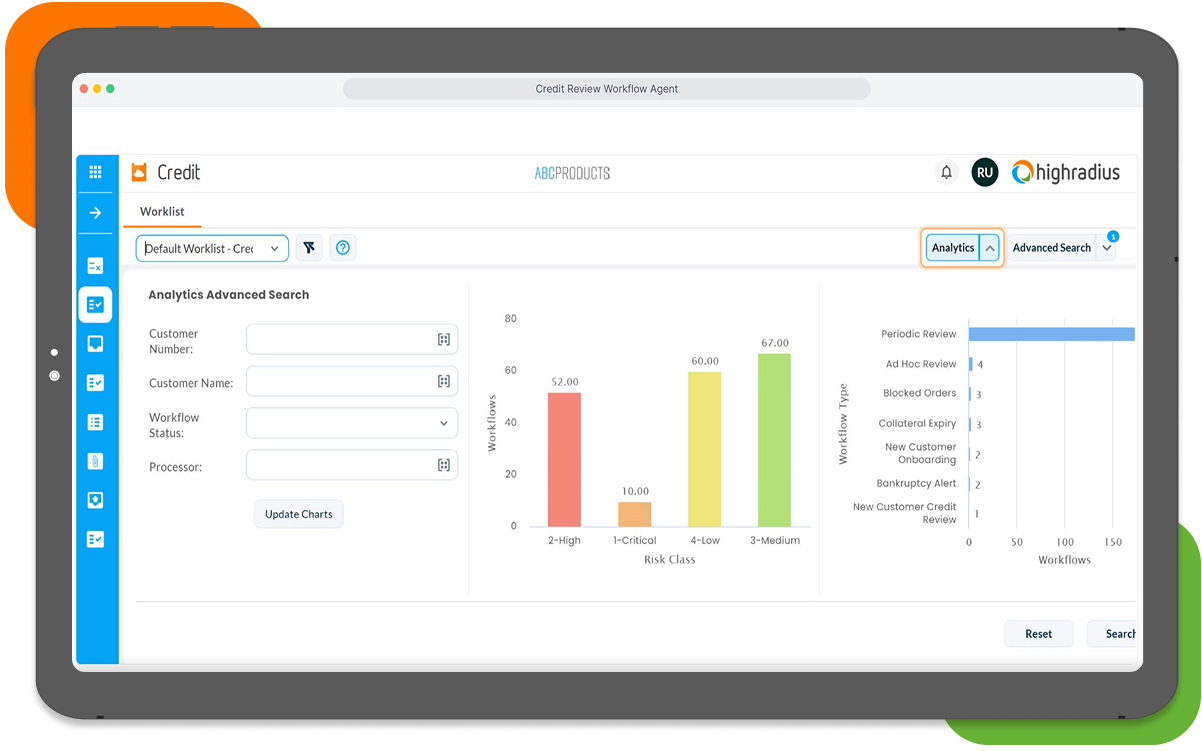

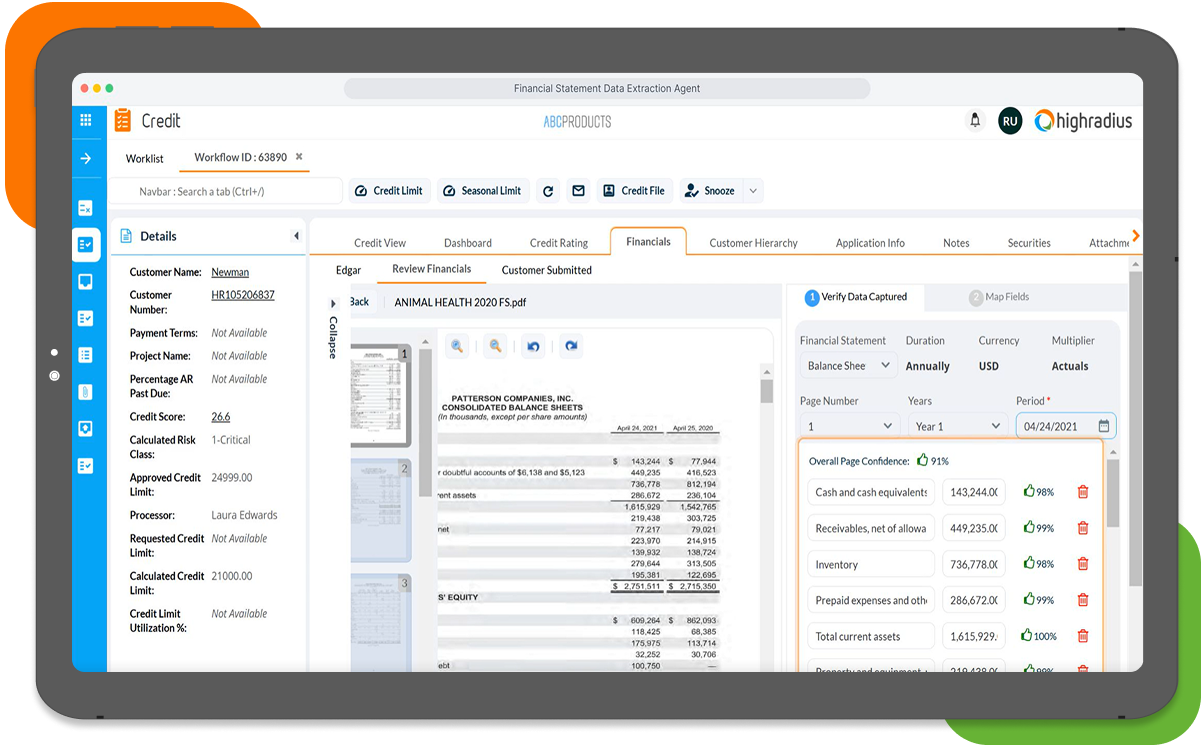

HighRadius Automated Credit Scoring Software helps businesses reduce default risk by replacing outdated scoring models with AI-driven risk evaluation. Built with predictive credit scoring capabilities, the solution enables businesses to lower bad debt exposure by up to 20%, accelerate credit limit decisions by 50%, and automate 80–90% of routine credit risk evaluations. By combining internal payment behavior, external credit intelligence, and configurable risk models, HighRadius helps businesses proactively identify risk and reduce up to $57 million in annual credit exposure.